BARBADOS PUBLIC WORKERS’ CO-OPERATIVE CREDIT UNION LIMITED

NON-CONSOLIDATED ANNUAL REPORT 2015

11

MANAGEMENT DISCUSSION AND ANALYSIS

management while at the same time adding valued customer

service. However, growth necessitated an increase in operating

expenses thus operating expenses (inclusive of tax on assets

of $1.4 million) increased by $2.4 million or 7.6 percent above

prior year.

OPERATING LEASES

Rent expenses increased during the year ending March 31,

2015 moving from $286 thousand in 2014 to $753 thousand

in 2015. This increase was directly attributed to expansion of

the Credit Union’s branch operations at the Six Roads location,

installation of two additional offsite ATMs and rental of office

space for staff at the Co-operators General Insurance’s building

on Collymore Rock.

STAFF COST

During the year, the Credit Union increased its staff complement

to strengthen its member services, financial reporting and risk

management functions as well as providing human resources

for its branch expansions.

In addition, incremental salary increases as well as higher

pension plan expenses also contributed to the increase in staff

costs. As a result, staff cost increased by $607 thousand or 5

percent over prior year.

TOTAL OPERATING EXPENSES

Total operating expenses for the year under review amounted

to $33.7 million, an increase of $2.4 million or 7.6 percent

above prior year. This included an amount of $1.4 million

which represented the 0.2 percent Asset Tax expense levied

by government on the assets of the Credit Union during the

financial year.

The effect of this levy largely resulted in the reported net income

being under that which was realized in the last financial year.

NET OPERATING INCOME

Net operating income inclusive of loan impairment expenses

increased by $863 thousand or 1.9 percent, to end the year

at $47.0 million. Loan impairment expense was $3.7 million,

a decline of $697 thousand or 15.8 percent below prior year.

This reduction was mainly due to a change in the ratio of non-

performing unsecured loans to non-performing loans with

security.

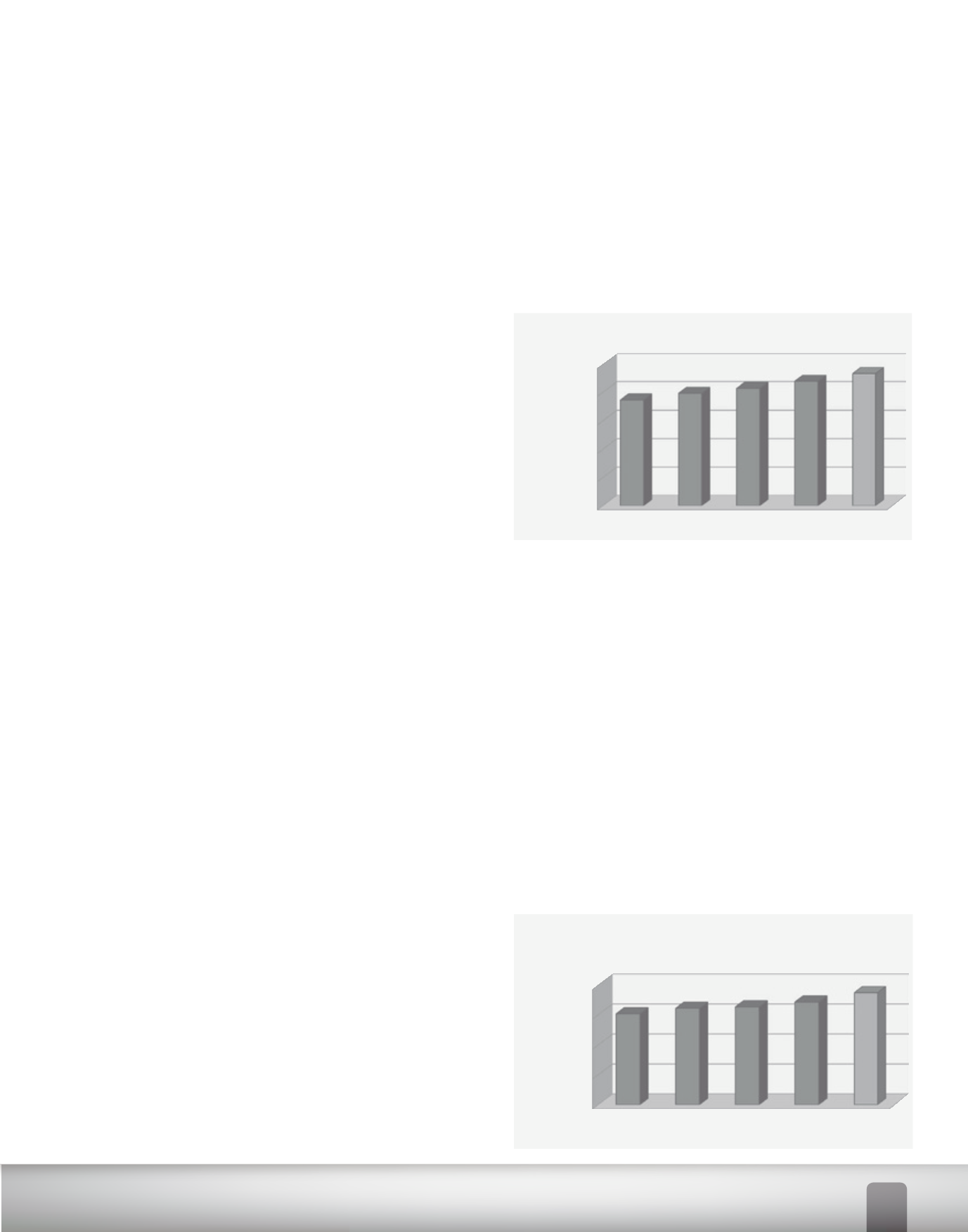

ASSETS

At year-end the Credit Union’s asset base amounted to $930.2

million, an increase of $53.6 million or 6.1 percent. During the

financial year ending March 31, 2015 cash resources decreased

by $15.5 million or 14.1 percent. This was mainly due to early

repayment of external debt so as to reduce interest expense.

In addition, financial investments classified as Held-to-maturity

increased by $5.4 million or 26.7 percent.

At the end of the financial year, the net loans and advances

to members rose to $746.5 million, inclusive of impairment

provision of $21.9 million, as compared to $684.3 million and

$21.3 million respectively at the end of the previous year. As it

was in the prior year, consumer loans was the major contributor

to loan growth in the reporting period.

ASSET QUALITY

Amid a climate of uncertainty and high job losses, the Credit

Union recorded an increase of 0.1 percent in its delinquency

ratio which ended the year at 6.7 percent compared to prior

year which was 6.6 percent. However, non-performing loans

increased by $4.2 million in comparison to the decrease of $4.6

million in the prior year.

The Credit Union will continue to work diligently with defaulters

to offer them alternatives and restructuring plans to enable

them to restore their loans to a state of normalcy.

In addition, support systems have been set up to help those

members who recently lost their jobs due to the retrenchment

exercise in the public sector. This has led to the restructuring of

loans to meet the needs of affected members who reached out

to the Credit Union for support.

0

200,000

400,000

600,000

800,000

1,000,000

2011

2012

2013

2014

2015

745,571 791,851

826,845

876,592

930,220

In BD$'000

Total assets

0

2,000

4,000

6,000

8,000

10,000

12,000

2011

2012

2013

2014

2015

6,791

9,939

11,993

10,427

9,606

In BD$'000

Net Income

0

200,000

400,000

600,000

800,000

2011

2012

2013

2014

2015

606,515 642,797 651,868 684,331

746,497

In BD$'000

Loans and advances